Minimis Safe Harbor Roof Replacement

Application Of Partial Asset Dispositions And The De Minimis Safe Harbor

Irs Tangible Propert Regulations

Tangible Property Regulations An Mps Cpa Presentation

Take Advantage Of New Tax Break For Repairs And Maintenance And Capitalized Assets

Safe Harbor Methods Personal Belongings Markham Norton Mosteller Wright Company Pa

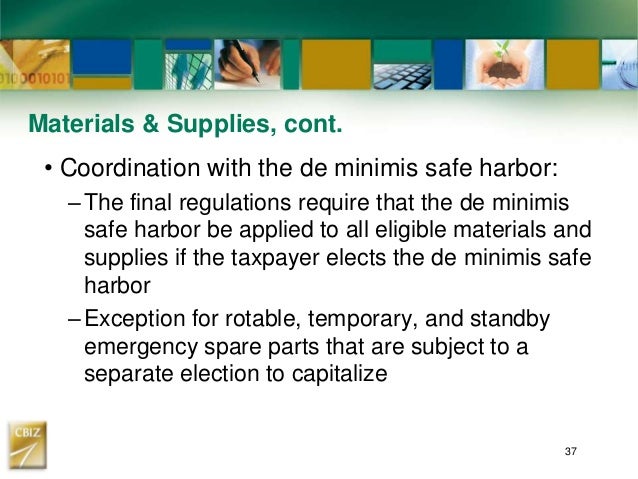

Key Aspects Of The New Tangible Property Regulations

Safe harbor for routine maintenance.

Minimis safe harbor roof replacement.

Are You Ready For The New Tangible Property Rules

Https Www Bdo Com Getattachment Cce22f03 0eb9 4dda 824e Fb8f9bdad1e8 Attachment Aspx

Https Www Claconnect Com Workarea Downloadasset Aspx Id 8716

N Overview Of Tangible Property Regulations N Greatest Impacts To Your Clients N Avoid The Traps Of The Temporary Regs N Action Steps To Prepare For Ppt Download

Optimizing Residential Real Estate Deductions Journal Of Accountancy

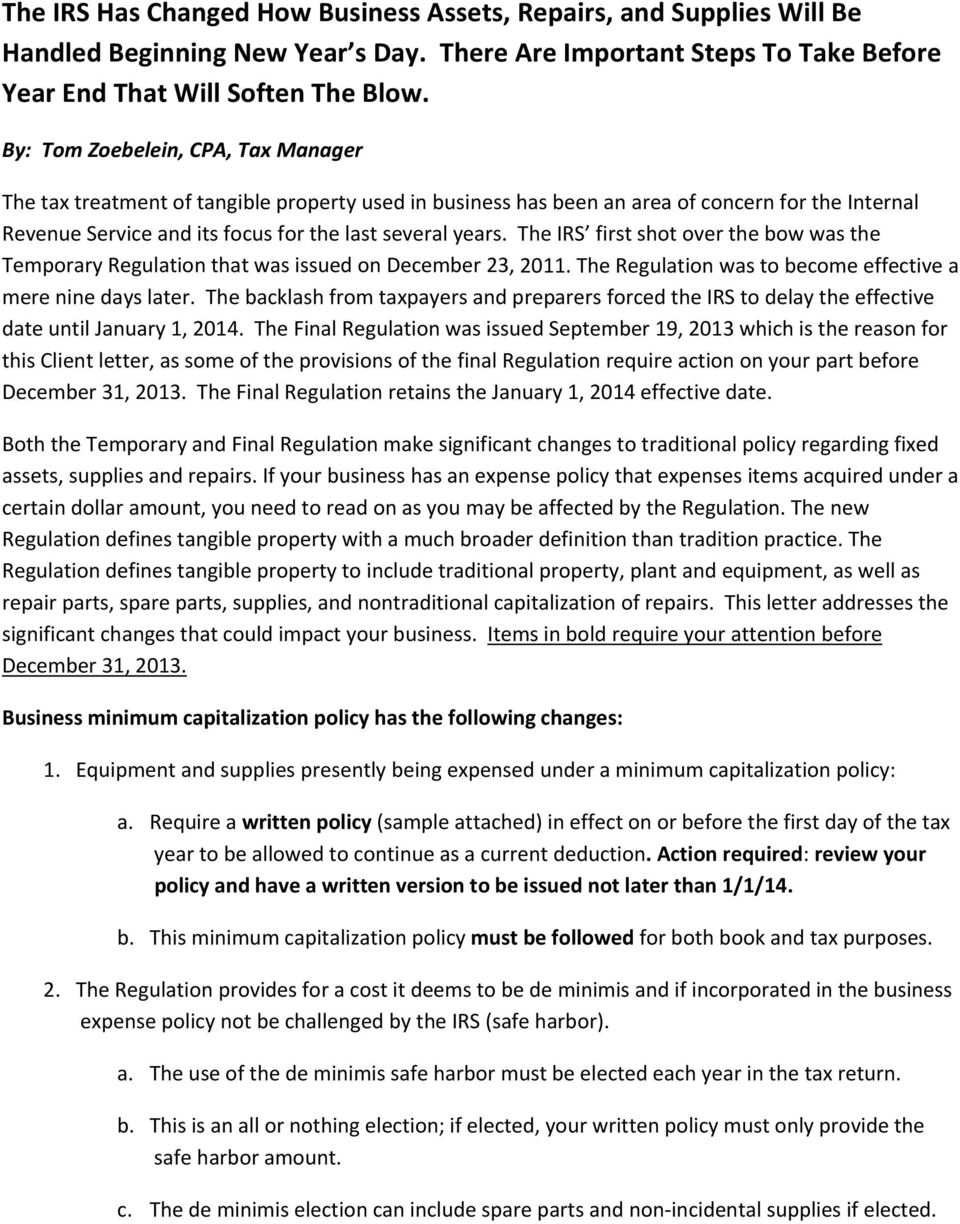

1 Equipment And Supplies Presently Being Expensed Under A Minimum Capitalization Policy Pdf Free Download

Https Www Cohencpa Com Cohensite Media Cohenredesign Image Gallery Events Documents Managing Capitalization Webinar Pdf

Capitalization Of Tangible Assets Xxxxxxxxxx Cpa And Xxxxxxx Cpa Ppt Download

Irs Increases Small Asset Expensing Safe Harbor Articles Resources Cla Cliftonlarsonallen

Put Firm Logo Or Letter Head Here Capitalization Of Tangible Assets Understanding The New Irs Regulations And What Client Name Needs To Do In Response Ppt Download

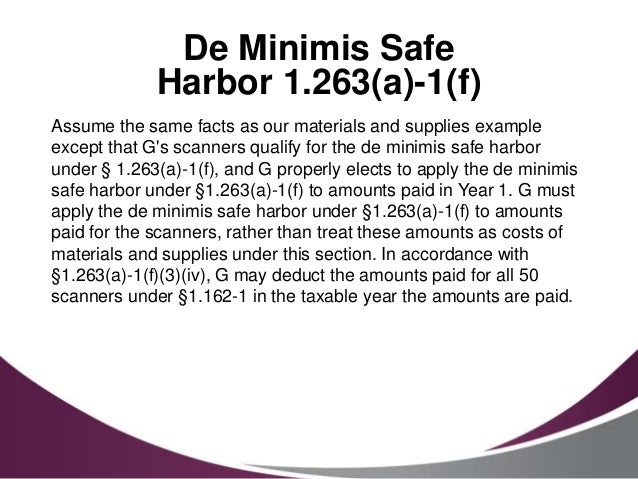

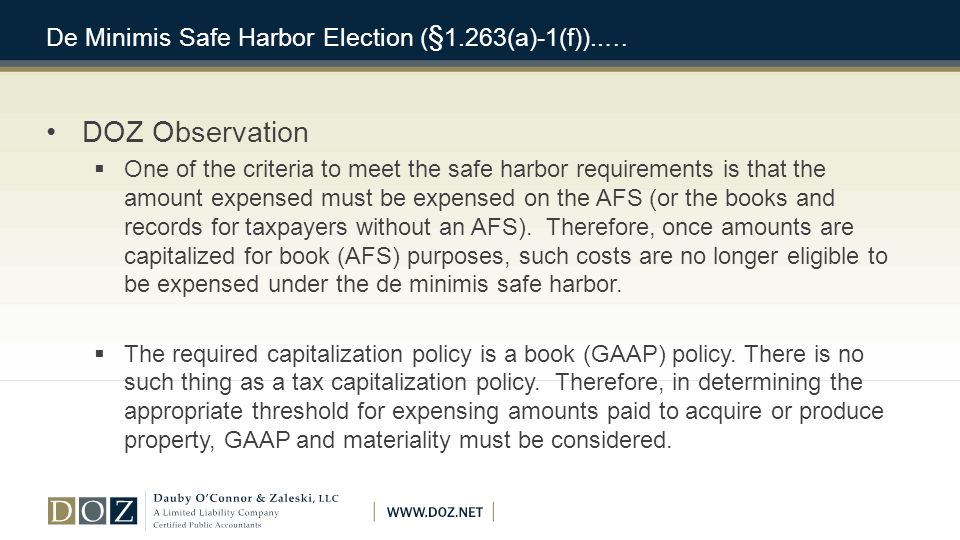

Final Tangible Property Dauby O Connor Zaleski Llc Doz Has Been In Business For 27 Years Has 150 Employees And Specializes In Ppt Download

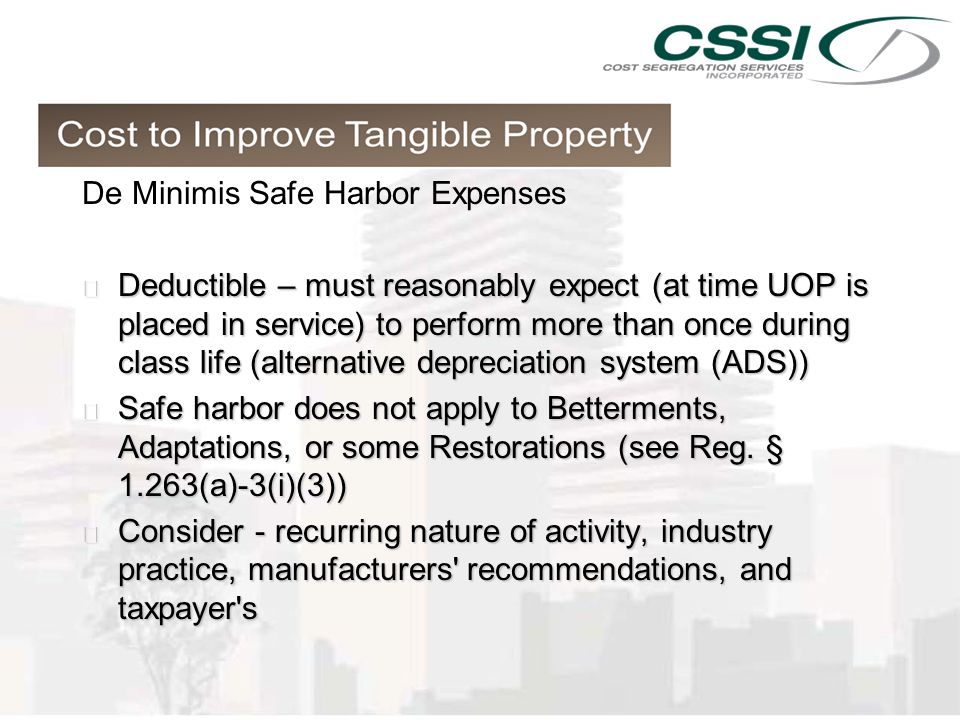

2014 Tax Savings Delivered Cost Segregation Tpr Implementation The Implementation Of The Tangible Property Regulations Cost Segregation Services Ppt Download

Engineered Tax Services Lunch Workshop

Depreciation Refresher 2017

Http Www Klcpas Com Wp Content Uploads 2014 11 Mcgowan Tpr Presentation Outline Pdf

Https Costsegexperts Com Wp Content Uploads 2019 10 Webinar Repair Regulation Fall 2019 Pdf

Https Assets Kpmg Com Content Dam Kpmg Pdf 2015 08 Tax Notes Repairs March 2012 Pdf

Understanding The Safe Harbor Rules And Keeping Money In Your Pocket

Routine Maintenance Safe Harbor

Complying With The Tangible Property Regulations Mission Impossible

Tax Guide Cpa For Real Estate Investors Real Estate Tax Accountant

Here Are Tax Tips For Hurricane Victims Khou Com

Ex 1 2 Ex1 Htm Exhibit 1 Exhibit

Farm Taxes Deducting Expenses An Overview Agfax

Source : pinterest.com